Introduction

The income statement for merchandising and manufacturing companies differs in the reporting of the cost of the merchandise (goods) available for sale and sold during the period.

This lecture will clarify how to prepare the income statement for a manufacturing company.

A manufacturing company has no need to prepare a manufacturing account, statement of production, or a cost sheet, before preparing the income statement.

The income statement remains the same except for the transfer of goods manufactured to a trading account to be treated as finished goods (at par with purchases).

Thus, the company that carries on manufacturing activity besides trading activity tends to prepare:

Manufacturing account (statement of production)Trading and profit and loss account (Income statement)Balance sheet (position statement)Preparing a manufacturing account shows the cost of materials consumed, productive wages, direct and indirect expenses of production, and the cost of finished goods produced.

Manufacturing account is debited with:

Opening stock of raw materials and purchase of raw materials during the year to closing stock of raw materials to get the raw materials consumedProductive wages and expenses to get the prime costfactory expenses to get the factory costWork-in-progress at the beginning of the year, work in progress at the end of the year, and the sale of scrap, if any, to get the cost of productionThe total cost of production is credited to the manufacturing account by giving a debit to the trading account.

ExplanationSome manufacturing companies prefer to transfer finished goods from the factory to the warehouse at an increased price, by adding a pre-set margin (called the manufacturing profit) to the production cost.

When preparing the income statement, the enhanced cost of production is taken into account to compute the cost of goods sold.

Goods are transferred to the trading account at a value which the business would have paid had these goods been bought from other manufacturers.

This approach ensures that the trading account shows a more realistic gross trading profit or loss

The manufacturing profit, i.e., the excess of the transfer value of goods manufactured over their actual production cost, represents the savings the company makes by manufacturing the goods

Given the rate for marking up the production cost; the accounting treatment would be as follows:

Debit: Manufacturing accountCredit: Profit and loss accountThe amount of markup is added to production cost, i.e., the manufacturing profit.

The above entry would increase the production cost, thereby reducing the gross profit disclosed by the trading account.

At the same time, crediting the profit and loss account by the amount of manufacturing profit does not affect the net profit.

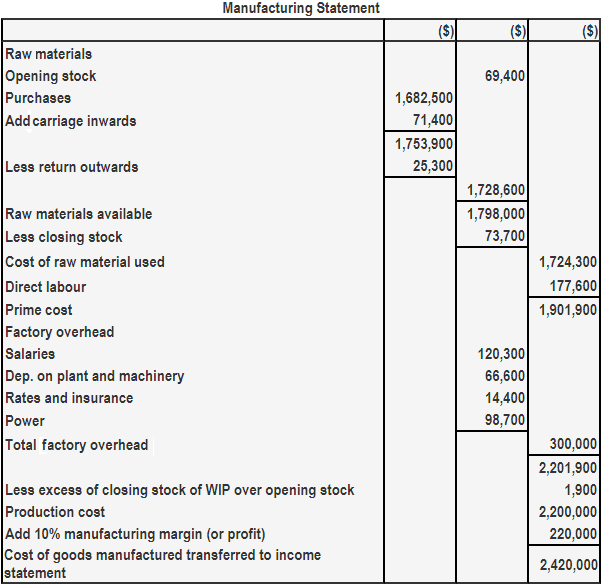

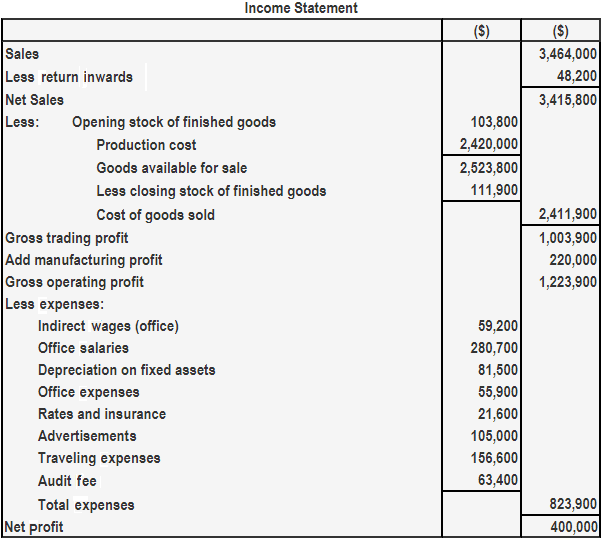

ExampleAssume that finished goods are transferred from the factory to the warehouse at production cost plus a 10% manufacturing profit. Show the relevant statements.

Solution